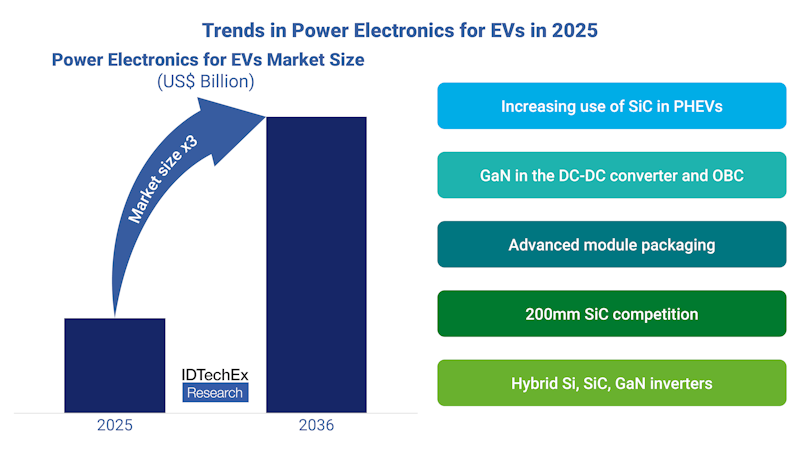

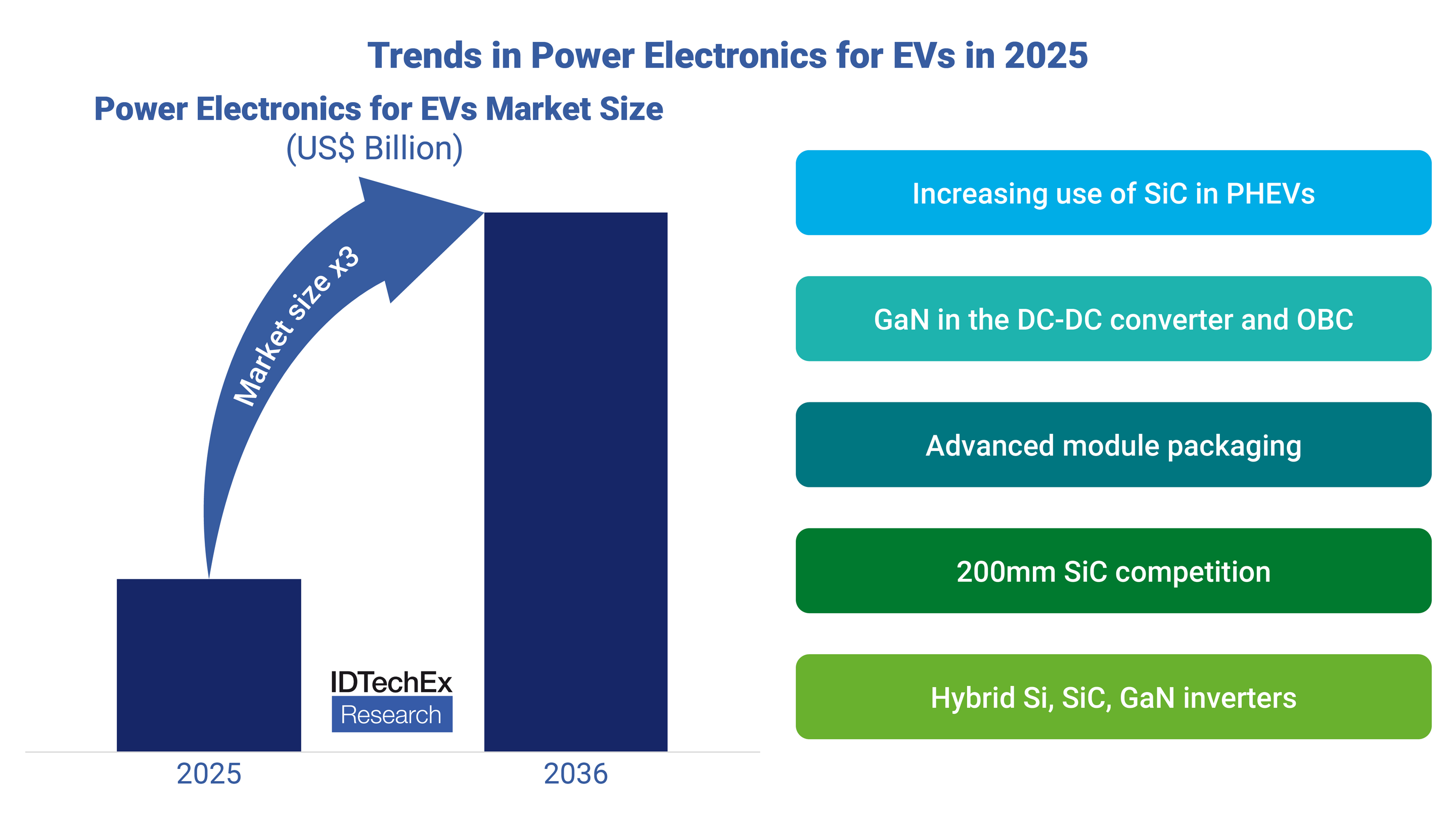

The electric vehicle power electronics market is set to exceed US$42 billion by 2036

2025 has been a turning point for the power electronics industry. Despite a slowdown in EV (electric vehicle) sales, IDTechEx forecasts a tripling in the market size of the power electronics for electric vehicles market, to US$42 billion by 2036. In IDTechEx's new report, "Power Electronics for Electric Vehicles 2026-2036: Technologies, Markets, and Forecasts", these trends are analyzed and used to forecast unit sales, market size, and US$ per kW.

IDTechEx forecasts the power electronics for EVs market to triple from 2025-2036, driven by technology trends in SiC and GaN. Source: Power Electronics for Electric Vehicles 2026-2036: Technologies, Markets, and Forecasts

Slowing EV Sales Will Not Slow Down SiC

While sales of battery-electric vehicles (BEVs) have slowed down at a global level, market penetration continues to grow. IDTechEx still considers the growth potential of SiC MOSFETs to be significant, with the global slowdown in BEV growth being offset by increased deployments of SiC MOSFETs for traction inverters in plug-in hybrid electric vehicles (PHEVs). Key OEMs and tier-one suppliers such as Toyota and Schaeffler have announced or released details of PHEV drivetrains using SiC MOSFETs.

This is another sign that SiC MOSFETs are moving towards market maturity. Even when only part of the drive cycles are purely electric-run, and battery sizes are smaller, companies are still choosing to integrate SiC MOSFETs into their EVs. Despite the re-engineering required for SiC inverters and the reduced revenue of device suppliers like Wolfspeed this year, it's clear that SiC MOSFETs are now a more mainstream choice for EVs than they were a year ago.

A major driver of the overall cost reduction of SiC MOSFETs is the increased competition of SiC wafer suppliers, with many companies now scaling up SiC wafer production, many at 200mm. The wafer costs of SiC far exceed those of Si products, and can be up to half the total cost of a SiC MOSFET die. Two years ago, only Wolfspeed and Coherent were capable of producing 200mm SiC wafers at scale. In 2025, Wolfspeed opened its 200mm SiC wafers to the wider market, and Infineon has scaled up 200mm SiC wafer production and delivered its first products based on its 200mm SiC platform earlier this year. Simultaneously, Chinese companies have validated and scaled up SiC wafer production, strengthening the supply chain of domestic OEMs such as Xiaomi and Li Auto.

High-Voltage Automotive GaN is Becoming a Reality

For years, the material properties of GaN have been predicted to revolutionize power conversion. Alongside the significant hype surrounding GaN in power supply units for data centers, the automotive industry should not be overlooked as a high-growth potential market for GaN. GaN is already used for LiDAR and low-voltage DC-DC converters, and we will finally be seeing the first deployment of GaN in the onboard charger (OBC) of the Changan Qiyuan E07. This is expected to enter the market with a power density in 2026, with GaN devices supplied by Navitas. Its stated power density of 6kW/L is far greater than the power densities seen in IDTechEx's research of existing OBCs, where 2kW/L is standard.

There are also multiple companies working on the design, control, and power semiconductors using GaN in the traction inverter, including VisIC Technologies, NXP, and Cambridge GaN Devices. While IDTechEx believes that commercial deployments of these will be later than in the OBC and DC-DC converter, the performance and potential cost savings of using GaN will drive technological maturity and market activity over the next ten years.

Other trends in Power Electronics: Hybrid Inverters, Embedded Power Modules

Hybrid inverters are a hot topic, and another key development that IDTechEx believes will drive wide bandgap semiconductor (WBG) adoption in electric vehicles. By paralleling a mixture of different transistors (Si IGBT, SiC MOSFET, GaN HEMT), one can optimize performance at all loads while minimizing cost. Gate drivers and load balancing are challenges for these, and the rapid decrease in SiC MOSFET cost could be a barrier to widespread adoption.

If a traction inverter could be produced at a competitive cost using only SiC MOSFETs, then the additional complexity of adding IGBTs in parallel would be less appealing. However, SiC MOSFETs are unlikely to ever reach cost parity with Si IGBTs, due to the temperatures required for crystal growth and the size of the boules grown compared to Si.

Embedded power modules, where the power semiconductor die is embedded into the printed circuit board (PCB), are another way to increase power density, while eliminating the need for wire bonds and reducing parasitics and ringing. Although this has not been mass-deployed in on-road vehicles as of October 2025, it's another trend that will drive overall power densities of power electronics upwards. Other trends in packaging and thermal management materials and methods are discussed further in IDTechEx's report.

Conclusions

Power electronics are fundamental to the world, whether it's in phone chargers, solar panels, or electric vehicles. This year has seen developments in the SiC supply chain, GaN technology, and other innovations that will drive value upwards for power electronics in electric vehicles, faster than growth in the electric vehicle market itself. IDTechEx forecasts Si, SiC, and GaN technologies by power conversion and yearly market size, as well as by EV application, in its new report: "Power Electronics for Electric Vehicles 2026-2036: Technologies, Markets, and Forecasts".

For more information on this report, including downloadable sample pages, please visit www.IDTechEx.com/PowerElec, or for the full portfolio of EV research available from IDTechEx, see www.IDTechEx.com/Research/EV.