Recent geopolitical tensions involving Iran have once again highlighted the vulnerability of global ammonia and fertilizer supply chains. The conflict has already contributed to higher natural gas prices, increasing production costs for conventional grey ammonia and fertilizer worldwide. The Gulf region is a major center for ammonia and fertilizer production and exports, with countries such as Quatar and Saudi Arabia supplying substantial volumes to global markets. Concerns surrounding regional stability, production reliability, and shipping routes through the Strait of Hormuz have increased uncertainty across the ammonia value chain. Similar disruptions were observed following Russia's invasion of Ukraine, which contributed to sharp fertilizer price increases and highlighted the risks associated with natural gas and global trade dependencies.

According to IDTechEx's report, "Ammonia Market 2026-2036: Technologies, Forecasts, Players", these developments are occurring as the ammonia industry undergoes transformation towards low-carbon production and applications. The report examines ammonia production, transportation, storage, and end-use applications, assessing the technologies, market drivers, and economic factors shaping the market between 2026 and 2036. Alongside traditional fertilizer demand, ammonia is increasingly attracting attention as a low-carbon fuel, and hydrogen carrier.

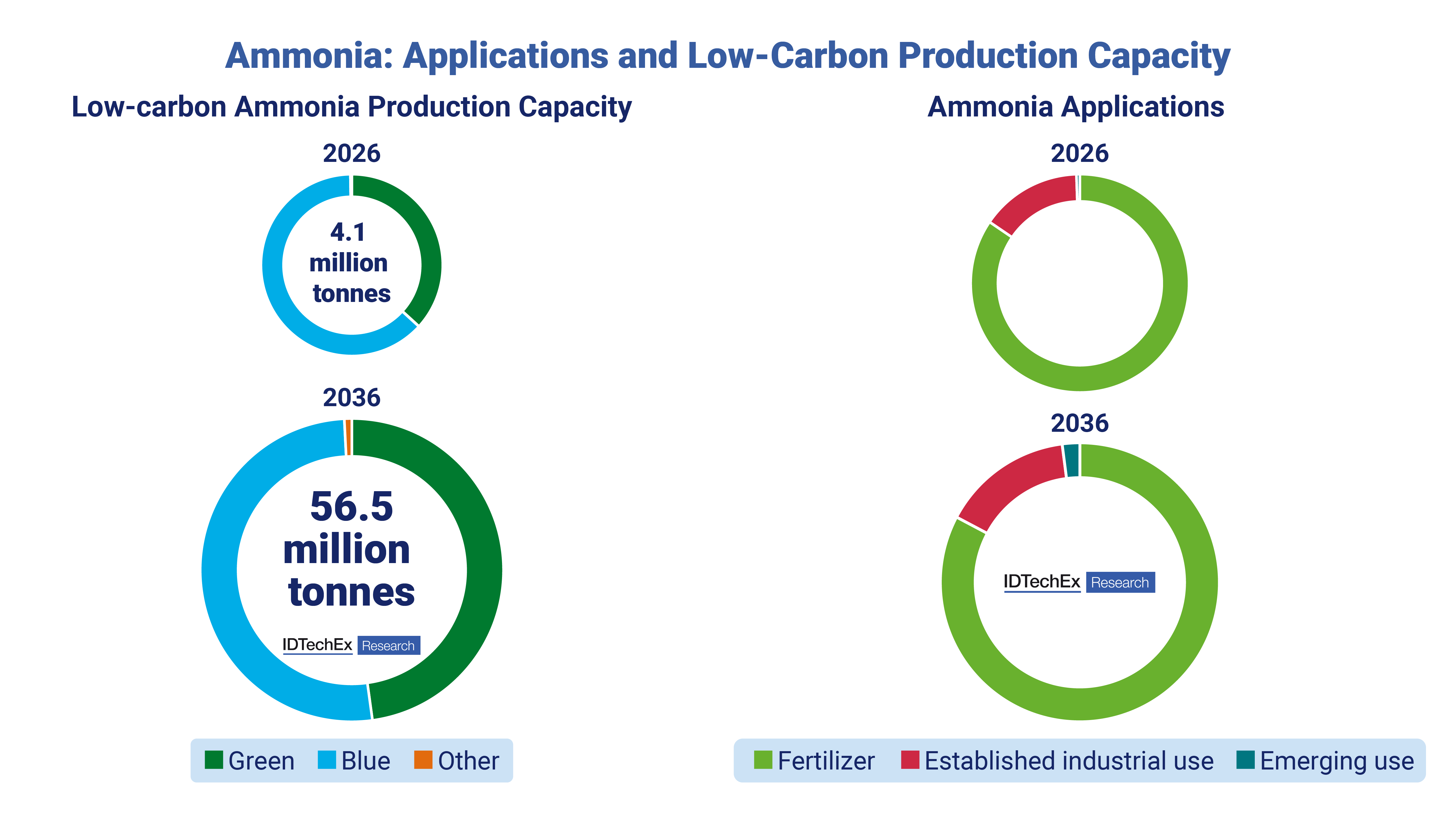

The low-carbon ammonia production capacity is forecast to reach over 56 million tonnes per year by 2036. Source: IDTechEx.

Ammonia is one of the world's most widely produced chemicals, with global production capacity exceeding 200 million tonnes annually. Fertilizer production remains the dominant application, underpinning global agricultural productivity and food security. However, the market is changing as governments and industries seek to reduce emissions, strengthen energy security, and develop new hydrogen infrastructure. This evolving landscape is driving investment into both green ammonia and blue ammonia production.

Conventional ammonia production relies on hydrogen sourced from natural gas before ammonia synthesis via the Haber-Bosch process. As a result, ammonia production costs remain highly sensitive to fluctuations in natural gas price and geopolitics. In contrast, green ammonia utilizes hydrogen produced through electrolysis powered by renewable electricity.

Historically, green ammonia has struggled to achieve cost parity with conventional production. Sustained increases in natural gas prices and governmental incentives will improve its competitiveness. However, a relatively small proportion of low-carbon announced projects are expected to reach final investment decision, reflecting ongoing uncertainty surrounding project economics, offtake demand, and future market development.

China remains the world's largest ammonia producer and consumer and is emerging as a major participant in low-carbon ammonia deployment. The country is developing a growing pipeline of green ammonia projects alongside broader investment in renewable energy and hydrogen infrastructure. Envision Energy's green ammonia facility in Chifeng is one example of large-scale investment currently underway. Blue ammonia currently represents a larger share of announced low-carbon ammonia capacity, partly because existing ammonia facilities can be retrofitted with carbon capture technologies while utilizing established infrastructure. Green ammonia, however, continues to attract increasing attention due to declining renewable electricity costs and expectations for long-term hydrogen demand growth.

The transition toward green ammonia faces some technical challenges. Conventional Haber-Bosch systems were designed for continuous. Renewable electricity generation, however, is inherently variable. This has led to growing interest in flexible Haber-Bosch systems capable of operating dynamically. One example is Topsoe's dynamic green ammonia plant in Denmark, which began operations in late 2025. The report assesses other developments in green and blue ammonia synthesis, such as electrolyzer developments and autothermal reforming.

Alongside large-scale projects, green ammonia is enabling interest in smaller-scale and more distributed production models. Conventional grey and blue ammonia plants are typically developed at very large scale due to the economics of fossil-based hydrogen production and ammonia synthesis. In contrast, green ammonia facilities can be deployed alongside dedicated renewable energy generation and may be economically viable at smaller scales in regions with favorable renewable resources.

Companies such as TalusAg are developing modular ammonia production systems designed to reduce transportation costs and improve fertilizer security. These facilities typically produce around one tonne of ammonia per day, a fraction of the output of conventional ammonia plants.

However, ammonia transportation can be costly due to its toxicity and the need for pressurization or refrigeration. In regions located far from major ports or ammonia production centers, transportation costs can represent a significant component of fertilizer pricing and local production. In the United States, incentives such as the 45V hydrogen production tax credit can further improve project economics. In many cases, transportation savings and supply chain resilience are proving to be as important as the environmental benefits associated with low-carbon ammonia production.

Emerging applications are contributing to growing interest in low-carbon ammonia, although adoption rates are expected to vary. Ammonia is receiving increasing attention as a marine fuel due to tightening emissions regulations within the shipping industry and the need for low-carbon fuels capable of supporting long-distance transport. Ammonia is also being explored as a hydrogen carrier, with ammonia cracking technologies attracting interest for hydrogen import and distribution applications. At the same time, decarbonization of existing fertilizer production remains a major driver for low-carbon ammonia deployment.

"Ammonia Market 2026-2036: Technologies, Forecasts, Players" provides detailed analysis of the technologies, infrastructure, project pipelines, and market dynamics shaping the future ammonia industry. Covering production, transportation, storage, ammonia cracking, bunkering infrastructure, and end-use applications, the report examines both the opportunities and challenges facing low-carbon ammonia as the industry responds to changing energy markets, geopolitical uncertainty, and decarbonization pressures.

For more information on this report, including downloadable sample pages, please visit www.IDTechEx.com/Ammonia, or for the full portfolio of energy and decarbonization-related research available from IDTechEx, see www.IDTechEx.com/Research/Decarbonization.